FoodExpoConnect Blog

Letter of Credit vs Documentary Collection: When to Use Each (2026 Decision Guide)

Letters of credit and documentary collections both reduce payment risk in food export — but the wrong choice costs you $200-500 per transaction in unnecessary bank fees. This decision guide with real scenarios shows exactly when each instrument makes sense.

Introduction: When a $35,000 Shipment Goes Wrong

You have shipped a container of organic ginger from Nigeria to a first-time buyer in Germany. The invoice is $35,000. The buyer asked for payment terms of "60 days after bill of lading" — effectively, they want the product now and will pay you later. You hesitated, but they are a large European importer with a professional website and polite emails.

Three weeks after the container arrives in Hamburg, the buyer stops responding. The ginger has already cleared customs. You have no payment, no leverage, and a $35,000 hole in your cash flow.

Now rewind. Instead of open account terms, you insisted on an irrevocable confirmed letter of credit. The buyer's German bank issued the LC. Your Nigerian bank confirmed it. When you presented the shipping documents — bill of lading, commercial invoice, phytosanitary certificate, packing list — your bank paid you within 5 business days. The buyer had zero opportunity to receive the goods without paying. Payment was guaranteed by two banks, not one buyer's promise.

The difference between these two scenarios is not luck. It is understanding when to use which trade finance instrument — and having the negotiating confidence to insist on the right one.

This guide explains exactly that.

What you will learn:

- Clear, plain-English distinction between letters of credit, documentary collections, and open account

- Real 2026 cost data for each instrument

- A decision framework based on buyer type, country risk, and transaction value

- What to watch for in LC terms that can trap you — and how to negotiate them out

- When to walk away from a deal rather than accept risky payment terms

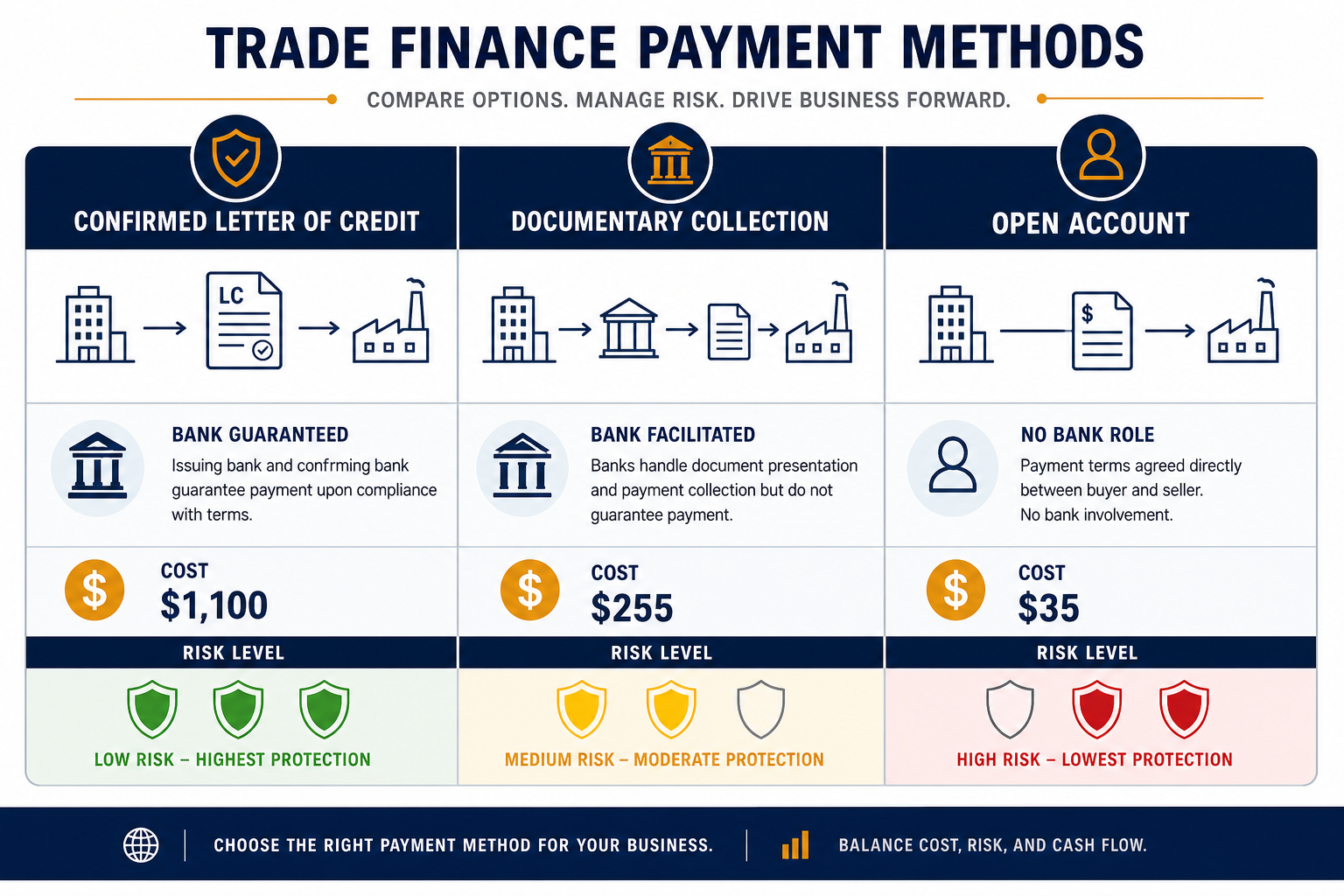

The Three Payment Methods: A Quick Comparison

International food export uses three main payment methods, arranged from most secure (for the exporter) to least secure:

| Feature | Confirmed LC | Unconfirmed LC | Documentary Collection | Open Account |

|---|---|---|---|---|

| Bank payment guarantee | Yes — two banks | Yes — buyer's bank only | No | No |

| Exporter risk | Very low | Low | Medium — buyer may refuse docs | High — trust only |

| Buyer risk | Medium — pays before seeing goods | Medium | Low — inspects docs before paying | Very low — goods first, pay later |

| Typical cost | 1.5-3% of value | 0.5-1.5% of value | $100-300 flat | $0 |

| Best for | New buyers, high-risk countries, large transactions | Established buyers in stable countries | Repeat buyers with good history | Long-term trusted relationships |

| Document compliance risk | High — strict compliance required | High — strict compliance required | Moderate — more flexible | None |

| Payment timing | At sight or deferred (per LC terms) | At sight or deferred | At sight or acceptance | Per agreement |

Letter of Credit (LC) — The Gold Standard

A letter of credit is a bank's irrevocable promise to pay the exporter, provided the exporter presents documents that strictly comply with the LC terms. The buyer's bank issues it. If confirmed, the exporter's bank adds its guarantee.

The mechanism: Buyer → applies to their bank → bank issues LC → exporter's bank advises/confirms it → exporter ships goods → exporter presents documents → bank examines documents → bank pays exporter → bank releases documents to buyer → buyer collects goods.

The critical feature: the bank pays based on documents, not on whether the buyer likes the goods. If your documents match the LC terms exactly, the bank must pay — even if the buyer has complaints about the product quality.

Documentary Collection (D/C) — The Middle Ground

A documentary collection uses banks as intermediaries to exchange documents for payment, but the banks make no payment guarantee. Two variants:

- Documents Against Payment (D/P or CAD): The buyer's bank releases shipping documents to the buyer only when the buyer pays. If the buyer refuses to pay, the documents stay with the bank and the exporter retains control of the goods — but must arrange their return or find an alternative buyer.

- Documents Against Acceptance (D/A): The buyer's bank releases documents against the buyer's signed promise to pay at a future date (typically 30-90 days). The exporter has a signed financial instrument but no bank guarantee of payment on the due date.

Open Account — Trust Only

The exporter ships goods and documents directly to the buyer. Payment is due per the agreed terms (typically 30-90 days after invoice or bill of lading date). The exporter has zero leverage once goods arrive. This method is common in intra-EU trade and among long-established relationships, but it is the riskiest for exporters dealing with new or overseas buyers.

Decision Framework: Which Instrument When?

The choice between LC, D/C, and open account depends on four variables. Run your transaction through this framework:

1. Buyer History

| Buyer Status | Recommended Instrument | Rationale |

|---|---|---|

| First transaction | Confirmed LC | No payment history. Protect yourself fully. |

| 2-3 successful LC transactions | Unconfirmed LC | Payment history established. Reduce cost by dropping confirmation. |

| 1+ year, 5+ transactions, no issues | Documentary Collection (D/P) | Trust established. Lower cost. |

| 2+ years, 10+ transactions, never late | Open Account | Relationship mature. Minimal risk. |

2. Country Risk

| Country Risk Level | Recommended Instrument | Example Countries |

|---|---|---|

| High (currency controls, political instability) | Confirmed LC only | Nigeria, Egypt, Pakistan, Lebanon, Ethiopia |

| Medium (stable but weak contract enforcement) | Confirmed LC or Unconfirmed LC | Kenya, Ghana, Bangladesh, Vietnam, Colombia |

| Low (OECD, strong legal systems) | Unconfirmed LC or D/C | Germany, UK, Netherlands, Japan, USA, Canada |

Critical note for African exporters: Your buyer's country risk matters more than yours for payment instrument selection. A German buyer paying a Ghanaian exporter via confirmed LC: the German bank's guarantee ensures payment regardless of what happens in Ghana. A Ghanaian buyer paying a German exporter: the exporter needs protection against Ghanaian country risk.

3. Transaction Value

| Transaction Value | Recommended Instrument | Reason |

|---|---|---|

| Under $10,000 | D/C or Open Account | LC fees consume too much margin |

| $10,000-25,000 | Unconfirmed LC or D/C | LC fees manageable, but evaluate if D/C sufficient |

| $25,000-100,000 | Confirmed LC (first time) / Unconfirmed LC (repeat) | Transaction size justifies LC cost |

| Over $100,000 | Confirmed LC | The cost of non-payment justifies full protection |

4. Product Specificity

| Product Type | Risk if Buyer Defaults | Recommended Instrument |

|---|---|---|

| Commodity (grains, raw nuts, bulk cocoa) | Low — easy to resell | Unconfirmed LC or D/C |

| Semi-processed (roasted coffee, shea butter) | Medium — branded packaging may limit resale | Confirmed LC |

| Custom/buyer-specific (private label, custom blend) | High — nearly impossible to resell | Confirmed LC + advance payment |

Real 2026 Cost Comparison

Here is what you actually pay for each instrument on a representative $35,000 food export transaction:

Scenario: $35,000 Organic Ginger — Nigeria to Germany

Confirmed LC (Irrevocable, at sight)

| Fee | Charged By | Amount | Notes |

|---|---|---|---|

| LC issuance fee | Buyer's German bank (0.3%) | $105 | Often passed to exporter in price negotiation |

| Advising fee | Exporter's Nigerian bank | $150 | Flat fee |

| Confirmation fee | Confirming bank (1.5% of LC value) | $525 | Adds second bank guarantee |

| Document examination | Exporter's bank | $200 | Per presentation |

| Courier/telex fees | Both banks | $120 | Document transmission |

| Total LC cost | $1,100 | 3.14% of transaction value |

Unconfirmed LC (same transaction)

| Fee | Charged By | Amount |

|---|---|---|

| LC issuance | Buyer's bank | $105 |

| Advising | Exporter's bank | $150 |

| Document examination | Exporter's bank | $200 |

| Courier | Both banks | $120 |

| Total LC cost | $575 |

Documentary Collection (D/P)

| Fee | Charged By | Amount |

|---|---|---|

| Collection order processing | Exporter's bank | $75 |

| Document handling | Buyer's bank | $100 |

| Courier | Both banks | $80 |

| Total D/C cost | $255 |

Open Account

| Fee | Amount |

|---|---|

| Wire transfer (Wise) | $35 |

| Wire transfer (traditional bank) | $40-70 |

| Total cost | $35-70 |

The real question is not what each instrument costs — it is what non-payment costs. On a $35,000 transaction, paying $1,100 for confirmed LC protection (3.14%) is significantly cheaper than absorbing a $35,000 loss. The LC fee is insurance. And on a 15% margin transaction, a single default wipes out the profit from 6-7 successful shipments.

Hidden Traps in LC Terms — and How to Spot Them

LCs protect you — but only if the terms are clean. Banks examine documents with ruthless precision. A single discrepancy — a misspelled consignee name, a missing date on a certificate, "ginger" instead of "organic ginger (Zingiber officinale)" — can give the bank grounds to refuse payment, even if the goods are perfect and already in the buyer's hands.

The 5 Most Common LC Traps

1. Impossible document requirements. If the LC requires an "inspection certificate issued by [specific agency]" but that agency does not operate in your country, you cannot comply. Verify every required document before accepting the LC. If any document is impossible for you to obtain, request an amendment before shipment.

2. Vague or contradictory descriptions. "Food grade quality" is vague. "Protein content minimum 12%, moisture maximum 8%, free from visible mould" is specific and verifiable. Insist on objective, measurable product descriptions. If the LC requires "top quality" without definition, it is unenforceable — but the bank will still reject documents if the description on your invoice does not match the LC.

3. Impossible shipping deadlines. If the LC requires shipment by 15 June but your container is not scheduled until 22 June, you will fail. Negotiate realistic shipment deadlines before accepting the LC. Amendment fees ($100-250) are cheaper than a failed presentation.

4. Expiry dates too tight. LCs have an expiry date — the last date you can present documents to the bank. Standard practice: expiry should be at least 21 days after the latest shipment date. If shipment is 30 June, expiry should be no earlier than 21 July. Tight expiry dates are a common trap: a 2-day delay in document preparation can push you past the expiry.

5. Confirmation by a bank you cannot verify. If the LC says "confirmed by [unknown bank]" and you cannot verify that bank's creditworthiness, the confirmation is worthless. Only accept confirmation from banks with international credit ratings (Moody's, S&P, or Fitch) or major international banks you recognise.

The Pre-Shipment LC Checklist

Before you accept any LC, verify these 7 points:

- ☐ LC is irrevocable (standard — revocable LCs are almost never used but confirm)

- ☐ All required documents are obtainable by you within the timeframes specified

- ☐ Product description matches exactly what your commercial invoice will say

- ☐ Shipment date is achievable given your production and logistics timeline

- ☐ Expiry date is at least 21 days after the latest shipment date

- ☐ If confirmed, the confirming bank is internationally rated and recognisable

- ☐ Partial shipments and transshipment are allowed (unless you specifically want to prohibit them)

When to Walk Away

Sometimes the right decision is to decline a transaction rather than accept risky payment terms. Walk away when:

- The buyer insists on D/A terms for a first transaction with a high-value shipment. Documentary collection with acceptance (D/A) is effectively open account with extra paperwork — you lose control of the goods and have only a signed promise of future payment.

- The buyer refuses an LC but the transaction is over $25,000 with a new buyer in a medium or high-risk country. A buyer who genuinely wants your product will accept reasonable payment protection. A buyer who resists all protection may not intend to pay.

- The LC contains terms you know you cannot comply with, and the buyer refuses to amend them. An LC with impossible terms is worse than no LC — it creates the appearance of protection while actually giving the bank grounds to reject your documents.

- The buyer's proposed bank is unknown, unrated, and the buyer refuses confirmation. If you cannot verify the issuing bank, and the buyer will not add confirmation from a recognised bank, the risk is unquantifiable.

Smart Stack: Tools for Payment-Secure Export

Payment platform for receiving LC proceeds: Once the bank pays under your LC, you need to receive the funds efficiently. Open a Wise Business account → — receive in 10+ currencies at mid-market rate, save 2-4% versus traditional bank FX on LC proceeds.

Buyer verification before issuing an LC: Before you invest time negotiating LC terms, verify the buyer exists and has a track record. Try Apollo.io → — verify company details, size, and industry presence. If a "major European importer" has 3 employees on LinkedIn, reconsider.

CRM to track LC milestones: Each LC has multiple deadlines — issuance, shipment, document presentation, expiry. Missing one kills the payment. Start Pipedrive free trial → — track each LC as a deal with automated deadline reminders.

B2B marketplace for finding verified buyers: Reduce the need for LCs by finding buyers with established track records. Search verified food buyers on Alibaba.com → — filter by verified supplier status and trade assurance coverage.

📊 Download the Payment Terms Decision Tree →

Interactive decision framework for choosing between LC, documentary collection, and open account terms. Risk assessment matrix by buyer country, relationship stage, and shipment value.

Free download — no email required.

The Bottom Line

The choice between letter of credit and documentary collection comes down to one question: can you afford to lose this shipment?

If the answer is no — and for most food exporters, the answer is no on any transaction above $10,000 with a new buyer — then pay for the LC. A confirmed irrevocable LC on a $35,000 transaction costs roughly $1,100. That is 3.14% of the transaction value. It is also the price of sleeping through the night while your container crosses the ocean.

If the buyer is established, the country risk is low, and you have multiple successful transactions behind you, documentary collection (D/P) saves $300-800 per transaction with manageable risk. And if the relationship spans years with perfect payment history, open account may be appropriate — but only after the buyer has earned that trust through performance, not promises.

One final rule that has served exporters well for decades: never let a buyer's payment-term request be the deciding factor in a deal you cannot afford to lose. If you need the sale badly enough to accept risky terms, you are already in a negotiation position where bad outcomes become likely. Build your buyer pipeline wide enough that you can walk away from bad terms. That — more than any LC clause — is the real payment protection.

Affiliate disclosure: FoodExpoConnect earns a commission when you sign up for Wise, Apollo.io, Pipedrive, or Alibaba.com through the links in this article. This does not affect the price you pay. We only recommend tools we have tested and that genuinely benefit food exporters.

Disclaimer: This article provides general information about trade finance instruments. It does not constitute financial, legal, or tax advice. Consult your bank and a qualified trade finance advisor for guidance specific to your transaction and jurisdiction.

Frequently asked questions

What's the difference between a letter of credit and documentary collection?

When should a food exporter use a letter of credit?

How much does a letter of credit cost in 2026?

What is a confirmed letter of credit and do I need one?

What documents do I need for a letter of credit in food export?

Quick facts

Published: 6/10/2026

Reading time: 10 min

Pillars: Trade Finance, Payment Security

Written by

Jean Marc Koffi

Co-authorJournalist & Export SpecialistLondon

Jean Marc Koffi is an MBA-trained trade specialist who connects African exporters to global buyers, with over $20M in contracts facilitated and expertise recognized by major trade organizations. Noted for rapid buyer network building, he is an experienced speaker and certified in trade facilitation, origin rules, and food safety.

Alocha Massamba

Co-authorFounder, Epifresh & FoodExpoConnectLondon

Alocha Massamba is the founder of Epifresh and FoodExpoConnect. He builds the technology, data and partnerships that connect African food producers and exporters to international buyers — with a focus on fresh-produce supply chains, cold-chain logistics, and the buyer-discovery platforms small and mid-size exporters need to compete with global incumbents.

Explore more export intelligence

Trade Policy • Market Access • Tariffs

July 24: Section 122 Dies, Section 338 Rises — Navigating the New US Tariff Landscape for Food Exporters

Section 122 import surcharge expires July 24 (effective US tariff rate drops from ~13% to ~7%), but Section 338 invokes 50% tariffs on Canadian dairy and alcohol. What food exporters must know about the new US tariff landscape.

Certification • Pricing Strategy • Market Access

5 Certifications Worth More Than a Price Cut in 2026

Stop competing on price. Organic, Fair Trade, Rainforest Alliance, B Corp, and SQF certifications can command 20-300% price premiums for African food exporters in 2026. Here is the ROI data for each.

Coffee Export • Market Access • EU Regulations

Coffee Export 2026: African Origins, Fair Trade Pricing & EU Market Access

Complete guide to coffee export from Ethiopia, Kenya and Rwanda — EUDR compliance, fair trade pricing, certification requirements, and how to access €12-18/kg EU buyer contracts in 2026.