FoodExpoConnect Blog

SeriesQ2 2026 Logistics SeriesContainer Shipping Rates Q2 2026: What Food Exporters Need to Know About Falling Freight Costs, Blank Sailings, and the Suez Return

Container rates have dropped 70% from pandemic peaks, Suez transits are resuming, and fleet overcapacity is 3-5%. But the rate bottom may be short-lived. Here's how food exporters should position their logistics strategy for Q2-Q3 2026.

For the first time in three years, food exporters are operating in a container shipping market that tilts in their favour. Spot rates on major trade lanes have fallen 45-55% from 2022 peaks. The Suez Canal — closed to most commercial traffic for nearly 24 months — is seeing selective carrier returns. And a wave of new vessel deliveries has created the first meaningful fleet overcapacity since before the pandemic.

But the good news comes with significant asterisks. The rate bottom may be short-lived. Blank sailings are rising as carriers fight to defend pricing. And the same geopolitical dynamics that have disrupted Red Sea shipping for two years could reverse the Suez reopening within weeks.

Here's what food exporters need to know to position their logistics strategy for Q2-Q3 2026 — and how to convert a buyer's market in container shipping into a durable competitive advantage.

What you'll learn:

- Current spot and contract rates across all major food export trade lanes

- The Suez reopening timeline, which carriers are returning, and what it means for your costs

- How blank sailings work — and how to protect your shipments from cancellations

- The fleet overcapacity situation and why it might not translate into sustained low rates

- A practical logistics strategy for food exporters in Q2-Q3 2026

Where Container Rates Stand: May 2026

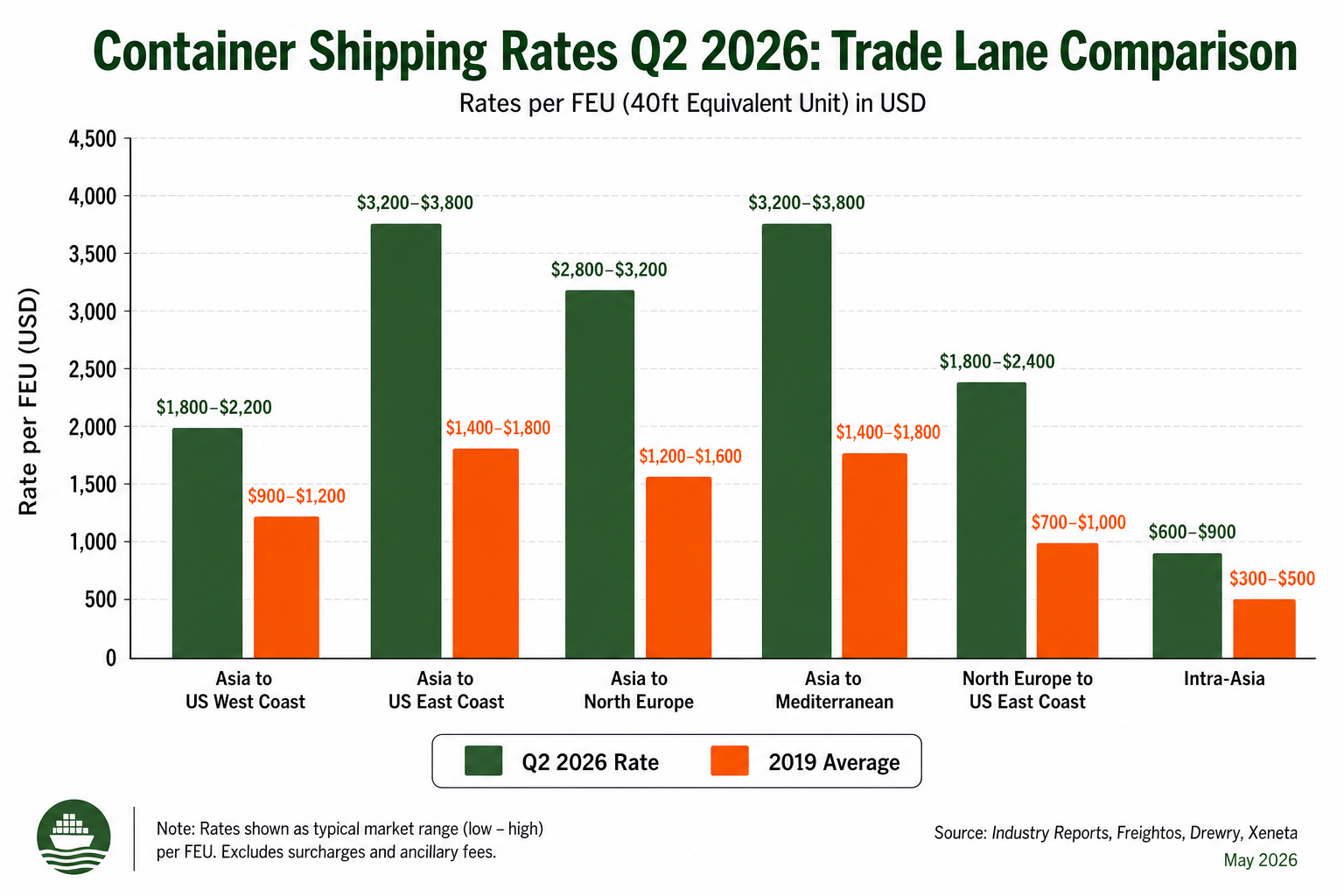

The container shipping market enters mid-May 2026 in a fundamentally different position than any point in the past five years. The numbers tell the story:

| Trade Lane | Spot Rate (May 2026) | vs. 2022 Peak | vs. 2019 Average |

|---|---|---|---|

| Asia → US West Coast | $1,800-2,200/FEU | -55% | +25% |

| Asia → US East Coast | $3,200-3,800/FEU | -45% | +35% |

| Asia → North Europe | $2,800-3,200/FEU | -50% | +120% |

| Asia → Mediterranean | $3,200-3,800/FEU | -45% | +130% |

| North Europe → US East Coast | $1,800-2,400/FEU | -35% | +15% |

| Intra-Asia | $600-900/FEU | -30% | +10% |

The pattern is clear: rates have normalised dramatically from pandemic-era extremes but remain elevated on routes affected by Red Sea disruption. The Asia-Europe corridor — where Suez avoidance has added 10-14 days of transit time and $400-700 per FEU in fuel surcharges — still trades at roughly twice 2019 levels, even as transpacific rates have largely returned to Earth.

The Contract vs. Spot Spread

The gap between contract and spot rates has narrowed but remains significant. Shippers who negotiated annual contracts in late 2025 locked in rates 15-25% below current spot levels. For food exporters who missed that window, the current spot market still offers manageable rates — but the strategic play is to negotiate mid-year contracts now while carrier leverage is weak.

Current contract rate benchmarks (for reference in your negotiations):

- Asia → USWC: $1,600-2,000/FEU (annual contract, 60-70% MQC commitment)

- Asia → USEC: $2,600-3,200/FEU

- Asia → North Europe: $2,400-2,900/FEU

Minimum quantity commitments (MQCs) have loosened significantly — carriers are now accepting 60-70% commitment levels versus the traditional 80%, reflecting their need to secure volume in an overcapacity market.

The Suez Return: 6% of Global Fleet Coming Back Online

The most significant structural shift in the container shipping market is the gradual return of Suez Canal transits. After 24 months in which virtually all Asia-Europe container traffic routed around the Cape of Good Hope, major carriers are now testing Suez passages.

Who's Returning and When

As of mid-May 2026:

- CMA CGM has begun selective Suez transits on Asia-Europe services, using naval escort coordination

- Maersk has announced a phased Suez return, starting with lower-value cargo and building toward regular service

- MSC remains primarily on Cape routing but is monitoring conditions

- Hapag-Lloyd, ONE, COSCO are taking a wait-and-see approach

The return is gradual by design. Carriers remember the chaos of early 2024, when vessels that had entered the Red Sea were forced to turn back after Houthi attacks escalated. No carrier wants to be the one that loses a vessel — or worse, crew — to a premature return.

What the Suez Return Means for Food Export Costs

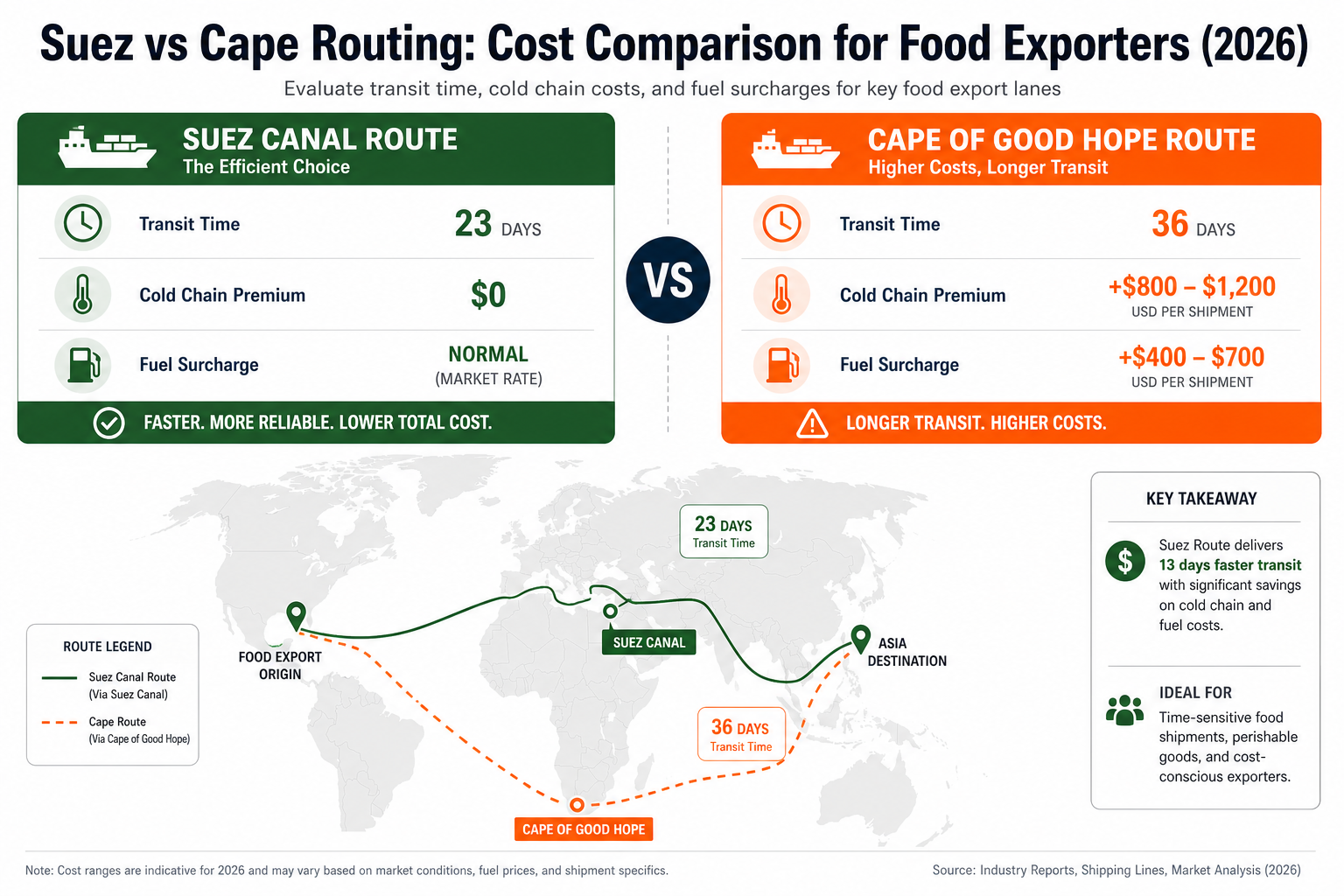

The Suez route versus the Cape route is not a marginal difference — it fundamentally changes the economics of food export logistics:

Transit time reduction: 23 days Asia-North Europe via Suez versus 36 days via Cape — a 13-day savings that is particularly valuable for perishable food exports.

Cold chain cost reduction: The additional 13 days of Cape routing costs roughly $800-1,200 per reefer container in additional power, monitoring, and insurance. Suez routing eliminates this premium almost entirely.

Fuel surcharge reduction: Cape routing adds $400-700 per FEU in bunker adjustment factor (BAF) charges. Suez routing reduces this to normal levels.

Capacity release: The return of Suez routing releases approximately 6% of global container fleet capacity back into the market. For every vessel that transits Suez instead of the Cape, roughly 1.3 vessels' worth of capacity is freed up (because the shorter route means each vessel can complete more round-trips per year).

For a mid-sized food exporter shipping 200 reefer containers annually from Southeast Asia to Europe, the switch from Cape to Suez routing represents approximately $160,000-240,000 in annual logistics cost savings — a 15-20% reduction in door-to-door shipping costs.

The Fragility Factor

The Suez return is real, but it is fragile. A single significant security incident — a successful attack on a commercial vessel in the Red Sea, a breakdown of the Yemen ceasefire, or a broader Middle East escalation — would reverse the return within days. Carriers have contingency plans to re-route via the Cape on 48 hours' notice.

For food exporters, this means: plan for Suez routing in your cost models, but build in Cape routing contingencies for your delivery commitments. The worst position is promising European buyers 23-day delivery times based on Suez routing and then having to explain 36-day delivery when the security situation shifts.

The Overcapacity Paradox: Why Low Rates Might Not Last

On paper, the container shipping market in 2026 should be a shipper's paradise. New vessel deliveries are adding 2.1-2.4 million TEU of capacity — an 8-10% increase in the global fleet. Global container demand is forecast to grow only 3-4%. The implied overcapacity is 3-5% after accounting for scrapping of older vessels.

But the container shipping market has a structural feature that prevents overcapacity from translating directly into sustained low rates: carrier consolidation and coordinated capacity management.

The Blank Sailing Playbook

Blank sailings — cancelled vessel departures — are the primary tool carriers use to manage capacity and defend pricing. In an overcapacity environment, carriers cancel sailings to create artificial scarcity. The mechanism is straightforward: if 10 vessels are scheduled on a route but demand only supports 8, carriers cancel 2 sailings rather than sailing all 10 at lower rates.

For food exporters, blank sailings create a specific set of problems:

- Schedule reliability declines: A sailing that was scheduled for Tuesday might be cancelled, with cargo rolled to the next sailing on Friday — a 3-day delay that can be catastrophic for perishable exports.

- Booking lead times extend: To secure space on a sailing that isn't cancelled, exporters need to book further in advance — typically 3-4 weeks versus 1-2 weeks in a balanced market.

- Peak season squeeze: Carriers concentrate blank sailings during shoulder seasons and run full schedules during peak season — when demand is high enough to support premium pricing.

The Carrier Profitability Floor

Major carriers — Maersk, MSC, CMA CGM, COSCO — remain profitable even at current rate levels, with operating margins of 15-25%. The estimated breakeven rate on the transpacific trade is $1,200-1,600 per FEU. Current spot rates of $1,800-2,200/FEU on the Asia-USWC route mean carriers have roughly $200-600 of margin per FEU before they start losing money.

This is important because it means carriers have room to let rates fall further without facing existential financial pressure. Unlike the 2016-2017 period, when several major carriers nearly failed and the industry consolidated, the 2026 market is one of comfortable profitability — not crisis.

For food exporters, this means: expect further rate softening, but don't expect a rate collapse. Carriers have the financial cushion and the coordination mechanisms to defend a pricing floor.

Lane-by-Lane Analysis for Food Exporters

Asia → Europe: The Suez Impact Lane

This is the trade lane most directly affected by the Suez return. Current spot rates of $2,800-3,200/FEU reflect the partial return of Suez transits — rates were $3,500-4,500/FEU in Q1 2026 when Cape routing was universal.

Forecast for Q2-Q3: If Suez transits continue expanding, Asia-Europe rates could fall to $2,200-2,800/FEU by late Q2. If the Suez return is disrupted, rates would spike back to $3,500-4,500/FEU within 2-3 weeks.

Strategy for food exporters on this lane:

- Book 60% of Q2-Q3 volume on contract at current rates

- Include a Suez routing clause: if Suez is available, the carrier must use it and pass through fuel savings

- Maintain relationships with at least two carriers on the route to preserve optionality

Asia → North America: The Demand-Dependent Lane

Transpacific rates have fallen furthest from pandemic peaks, with Asia-USWC rates approaching 2019 levels. The demand picture is weak — Q1 2026 import volumes trailing 7% behind Q1 2025, and March 2026 volumes projected 16.8% below March 2025.

Forecast for Q2-Q3: Sideways to slightly soft through April-May, with moderate 10-20% upward pressure if early peak-season bookings materialise in June. The wildcard is tariff policy — a Supreme Court ruling on IEEPA tariffs could trigger a front-loading surge that would spike rates.

Strategy for food exporters on this lane:

- Take advantage of current low rates to lock in annual contracts for 2026-2027

- Build flexibility into booking windows — the 7% demand gap means last-minute space is generally available

- If you export perishables that require reliable scheduling, negotiate guaranteed-loading provisions even if they carry a premium

Latin America → North America: The Regional Stability Lane

This trade lane has been the most stable, with rates fluctuating within a narrower band than the headline-grabbing Asia-Europe and transpacific routes. The proximity of Latin American food exporters to the US market — particularly for Mexican, Central American, and Caribbean exporters — provides a structural advantage that container rate volatility does not erase.

Forecast for Q2-Q3: Flat to slightly lower pricing. The US driver capacity squeeze — enforcement of CDL English-proficiency and residency rules could remove 10-15% of trucking capacity — could create port congestion that feeds back into container rates, but the effect is likely modest.

Strategy for food exporters on this lane:

- This is a good lane for spot market utilisation — the short transit times mean less exposure to rate volatility

- Monitor US port labour negotiations — ILA and ILWU contracts are active through 2027-2028, but local disputes can still disrupt specific ports

- Consider nearshoring strategies that reduce container shipping dependency entirely for US market access

Africa → Europe: The Cape-Advantaged Lane

African food exporters on the Atlantic coast — West Africa, Southern Africa — have a structural advantage in the current shipping environment. Cape of Good Hope routing, which adds 10-14 days and $800-1,500 per container for Asia-Europe shipments, is the default routing for West African exports to Europe. There is no premium to pay, because the Cape is the natural route.

Forecast for Q2-Q3: Stable to slightly improving rates as global container capacity expands and carrier competition for African export cargo increases.

Strategy for food exporters on this lane:

- Leverage the Cape routing advantage in negotiations with European buyers — your shipping costs are structurally lower than Asian competitors on a door-to-door basis

- Invest in cold chain infrastructure to close the quality gap with shorter-transit competitors

- Monitor the African Continental Free Trade Area implementation — improved intra-African logistics corridors could open regional markets that reduce dependency on long-haul container shipping

The Fuel Factor: Bunker Prices and Environmental Surcharges

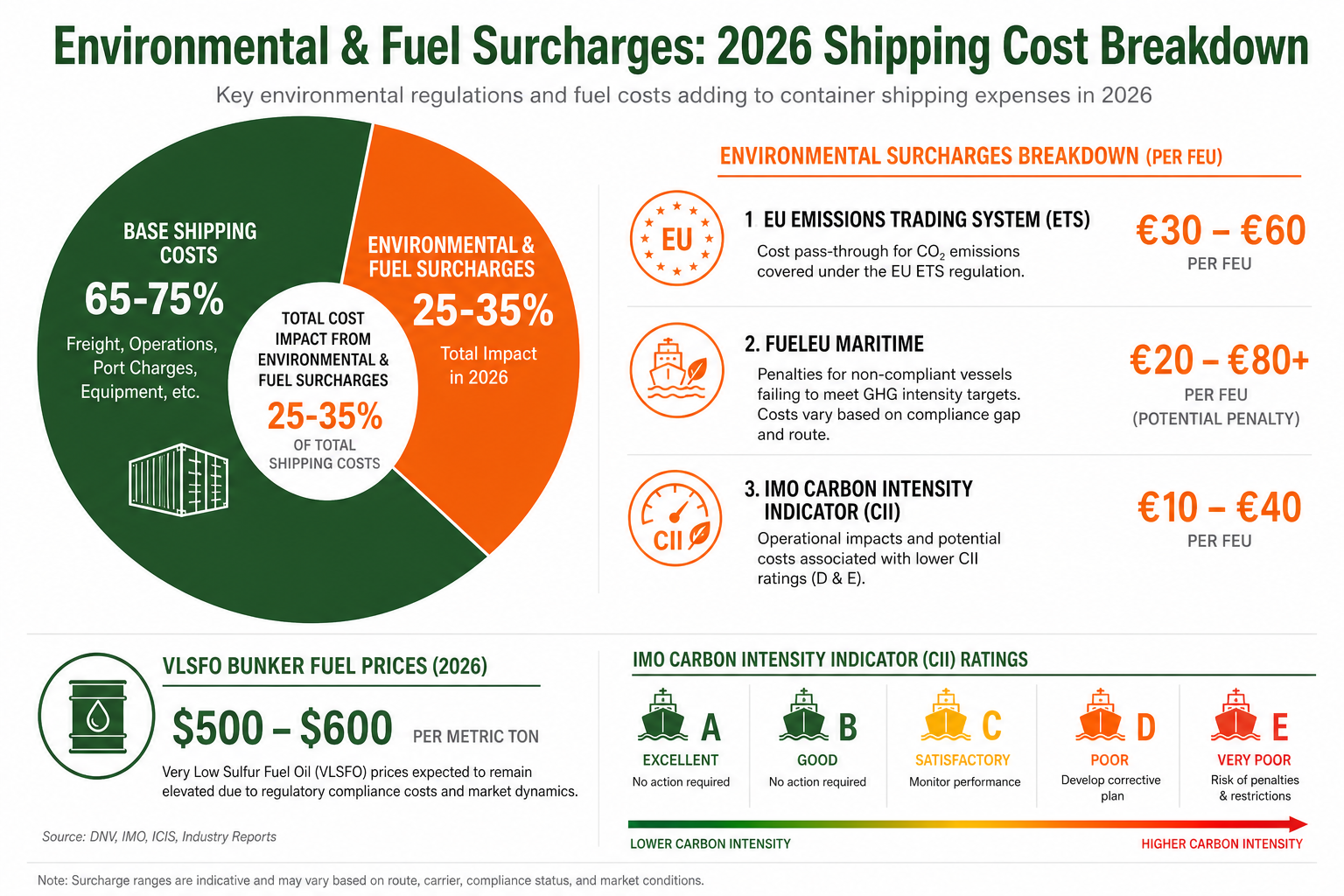

Container shipping rates do not exist in a vacuum — fuel costs, which typically represent 30-50% of vessel operating costs, flow directly into the bunker adjustment factor (BAF) that appears on every freight invoice.

Bunker fuel prices in May 2026 are moderate by historical standards — roughly $500-600 per metric ton for VLSFO (very low sulphur fuel oil), compared to $800-1,000 during the 2022 energy crisis. The moderate fuel price environment is one of the factors enabling the current rate softness.

But environmental regulations are adding a new layer of fuel-related costs:

- EU Emissions Trading System (ETS): Applicable to shipping from 2024, the EU ETS adds an estimated €30-60 per FEU for Asia-Europe voyages, with costs rising as the allowance phase-in progresses

- FuelEU Maritime: Entering force in 2025, this regulation imposes penalties for vessels that do not meet greenhouse gas intensity targets, adding incremental costs that carriers pass through to shippers

- IMO Carbon Intensity Indicator (CII): Vessels rated D or E face operational restrictions, incentivising slow steaming (which reduces fuel consumption but extends transit times)

For food exporters, the environmental surcharge layer means that even as base freight rates fall, total door-to-door costs may not fall proportionally. When negotiating contracts, ask carriers to break out environmental surcharges separately from base freight — this transparency will help you understand the true cost structure and negotiate more effectively.

Practical Logistics Strategy for Q2-Q3 2026

1. Split Your Volume Strategy

The single most effective logistics strategy in the current market is volume splitting: lock 60-70% of your projected volume on annual or semi-annual contracts at current favourable rates, and keep 30-40% on the spot market.

The contract volume gives you cost predictability and guaranteed space for your core business. The spot volume gives you upside if rates continue to fall — and flexibility to shift between carriers as service reliability fluctuates.

2. Negotiate GRI Rollback Clauses

General rate increases (GRIs) are carrier attempts to raise rates across a trade lane — typically $300-600 per FEU. In an overcapacity environment, most GRIs fail to hold for more than a few weeks before rates drift back down.

When negotiating contracts, include a clause that resets your contract rate if a GRI fails to hold for more than 14 days. The clause should specify: if the carrier implements a GRI and the spot market rate (as measured by an agreed index like the Freightos Baltic Index) falls back to pre-GRI levels within 14 days, your contract rate reverts.

3. Confirm Suez vs. Cape Routing on Every Booking

Do not assume your cargo is routing via Suez just because the carrier has announced Suez returns. Ask for specific routing confirmation on every booking. If Cape routing is used, ask for the cost differential versus Suez — you may be paying BAF charges that assume Suez routing even when your container is going around the Cape.

4. Build Multi-Carrier Relationships

The dissolution of the 2M Alliance (Maersk + MSC) in February 2025 and the restructuring of carrier alliances has increased competition and options for shippers. Maintaining relationships with at least two carriers — ideally across different alliances — gives you leverage in negotiations and backup options when one carrier blanks a sailing or shifts routing.

5. Invest in Visibility Tools

The container shipping market in 2026 is information-rich — real-time rate data, vessel tracking, port congestion metrics, and schedule reliability scores are all available through platforms like Freightos, Xeneta, and various freight forwarder dashboards. Exporters who invest in visibility tools make better booking decisions than those who rely on their forwarder's weekly rate sheet.

6. Factor Logistics Into Your Pricing and Contracts

The most common mistake food exporters make is treating logistics as a separate function from commercial strategy. In a market where shipping costs can swing 20-30% within a quarter, logistics cost volatility should be built into your export pricing and buyer contracts.

Consider:

- Freight adjustment clauses in long-term supply contracts that pass through a portion of rate changes

- Incoterms selection that allocates freight cost risk appropriately — FOB for exporters who want to minimise freight exposure, CIF for exporters who can manage freight procurement competitively

- Buffer pricing that builds in 10-15% freight cost headroom above current spot rates to protect against spikes

Conclusion: Use the Buyer's Market While It Lasts

The Q2 2026 container shipping market is the most favourable for food exporters since 2019. Rates are down, capacity is up, and carrier leverage is diminished. The Suez return — if it holds — will further reduce costs on the Asia-Europe corridor that has been the most disrupted trade lane.

But the structural dynamics of container shipping — carrier consolidation, coordinated capacity management, and geopolitical fragility — mean this buyer's market is not permanent. The exporters who use this window to lock in favourable contracts, build multi-carrier relationships, and invest in logistics visibility will have a structural cost advantage when the market eventually turns.

The food exporters who treat logistics as an afterthought — booking at spot rates, relying on a single carrier, and hoping for the best — will find themselves squeezed when the cycle shifts, as it inevitably does.

Jean-Marc du Plessis is a food export strategist and MBA graduate of INSEAD with 14+ years of experience in African agricultural exports and global commodity supply chains. He advises food exporters on logistics strategy, trade policy compliance, and market entry.

Shipping food products internationally? Connect with verified freight forwarders and logistics partners on FoodExpoConnect — access logistics providers experienced in food export from 18+ countries across Africa, Asia, and Latin America.

Frequently asked questions

What are current container shipping rates in Q2 2026?

Is the Suez Canal open for container shipping in May 2026?

Should food exporters lock in contract rates or use spot market in 2026?

How does the Suez reopening affect food export shipping costs?

What are blank sailings and how do they affect food exporters?

Quick facts

Published: 5/17/2026

Reading time: 12 min

Pillars: Shipping, Trade Routes

Written by

Jean Marc Koffi

Co-authorJournalist & Export SpecialistLondon

Jean Marc Koffi is an MBA-trained trade specialist who connects African exporters to global buyers, with over $20M in contracts facilitated and expertise recognized by major trade organizations. Noted for rapid buyer network building, he is an experienced speaker and certified in trade facilitation, origin rules, and food safety.

Alocha Massamba

Co-authorFounder, Epifresh & FoodExpoConnectLondon

Alocha Massamba is the founder of Epifresh and FoodExpoConnect. He builds the technology, data and partnerships that connect African food producers and exporters to international buyers — with a focus on fresh-produce supply chains, cold-chain logistics, and the buyer-discovery platforms small and mid-size exporters need to compete with global incumbents.

Series

More in Q2 2026 Logistics Series

Ocean Freight Q2 2026: Why Container Rates Are Dropping on Some Routes and Surging on Others

A tale of two shipping markets: transpacific rates have collapsed 70% from their 2022 peak while Asia-Europe spot rates surge 40% on Iran disruption. Here's what it means for food exporters and how to route around the volatility.

How the Red Sea Crisis Is Reshaping Global Food Export Routes in 2026: What Every Exporter Must Know

The Red Sea shipping crisis is adding $1,500 per container and 14 extra days to food export routes. Here's how smart exporters are adapting their logistics, insurance, and buyer relationships.

How the Middle East Conflict Is Disrupting Global Food Trade: What Every Exporter Must Know in 2026

The 2026 Iran war and Strait of Hormuz closure have shattered global shipping routes, spiked freight costs by 300%, and triggered a fertiliser crisis. Here is what food exporters need to do right now.

Explore more export intelligence

Export Operations • Finance • Risk Management

Letter of Credit vs Documentary Collection: When to Use Each (2026 Decision Guide)

Letters of credit and documentary collections both reduce payment risk in food export — but the wrong choice costs you $200-500 per transaction in unnecessary bank fees. This decision guide with real scenarios shows exactly when each instrument makes sense.

Export Operations • Tools & Software • Food Manufacturing

Best ERP Software for Small Food Manufacturers in 2026: MRPeasy vs Odoo vs Katana Compared

Running a food manufacturing business on spreadsheets and sticky notes costs you 15–20% of production capacity in planning errors, inventory waste, and compliance failures. We compared the top four ERP systems built for small food manufacturers — here's which one actually fits your operation.

Export Strategy • Pricing & Profitability • African Exports

Pricing Premium for African Food Exports: How to Capture 25-40% Margin Uplift Through Premium Positioning (2026)

African food exporters routinely leave 25-40% margin on the table by selling commodity-grade. We break down the premium positioning strategies — certification, storytelling, packaging, and direct buyer relationships — that turn $4/kg cashews into $12/kg specialty product.