FoodExpoConnect Blog

SeriesPayments & FX for ExportersBest Payment Platforms for Food Exporters in 2026: Wise vs Payoneer vs Banks (Real Fee Comparison)

International payment fees quietly eat 3-7% of your export revenue. We tested Wise, Payoneer, and traditional banks with real transaction scenarios. Here's which platform saves you the most money — and when to use each one.

Introduction

Here's a number that should make every food exporter uncomfortable: on a $10,000 shipment of Ghanaian cashew nuts to a German buyer, the average exporter loses $300 to $700 in payment fees. Not in shipping. Not in tariffs. In simply receiving the money.

That's 3-7% of your revenue. Gone. To bank fees, exchange rate markups, and intermediary charges that nobody explains on your statement. And most exporters don't even know they're losing it — the fees are buried in the exchange rate, invisible unless you check the mid-market rate against what your bank actually gave you.

In 2026, this is a solvable problem. Digital payment platforms have made international money movement dramatically cheaper — but the landscape is confusing. Wise, Payoneer, Airwallex, traditional banks, specialist FX brokers... which one actually saves you money for your specific export pattern?

I've tested the major platforms with real transaction scenarios for food exporters. Here's the unvarnished comparison. And yes — there are affiliate links in this article (clearly marked). If you sign up through them, FoodExpoConnect earns a commission at zero cost to you, which funds our free exhibitor database. Fair?

What you'll learn:

- Exact fee breakdowns for 5 export payment scenarios ($500 to $50,000)

- Wise vs Payoneer vs traditional banks — real numbers, not marketing claims

- Which platform to use for which type of buyer (European vs Asian vs Middle Eastern)

- How to handle currency exchange risk without a finance degree

- The one thing traditional banks don't want you to know about their exchange rates

The Hidden Killer: Exchange Rate Markup

Before we compare platforms, you need to understand the biggest fee you're probably paying without knowing it: the exchange rate markup.

When a German buyer sends you €9,200 for your $10,000 invoice, your bank doesn't convert it at the rate you see on Google. They add a spread — typically 2-4% above the mid-market rate. On €9,200, a 3% markup costs you $300. And nowhere on your statement does it say "exchange rate fee: $300." It's invisible.

How to check if you're being ripped off:

- Google "EUR to USD" when your payment arrives. That's the mid-market rate.

- Look at the rate your bank actually applied. It's almost certainly worse.

- Multiply the difference by your invoice amount. That's your hidden fee.

If the difference is more than 1%, you're overpaying. If it's more than 2%, you're being actively exploited. Most traditional banks fall in the 2-4% range.

Wise uses the mid-market rate — the same one you see on Google — and charges a separate, transparent percentage fee. You can see exactly what you're paying before you accept a payment. This single difference is why Wise saves exporters hundreds of dollars per transaction. Try Wise Business → — free to open, no monthly fees, mid-market exchange rate.

Scenario-by-Scenario Comparison

Let's run real numbers. These are actual fee calculations for common food export scenarios as of May 2026.

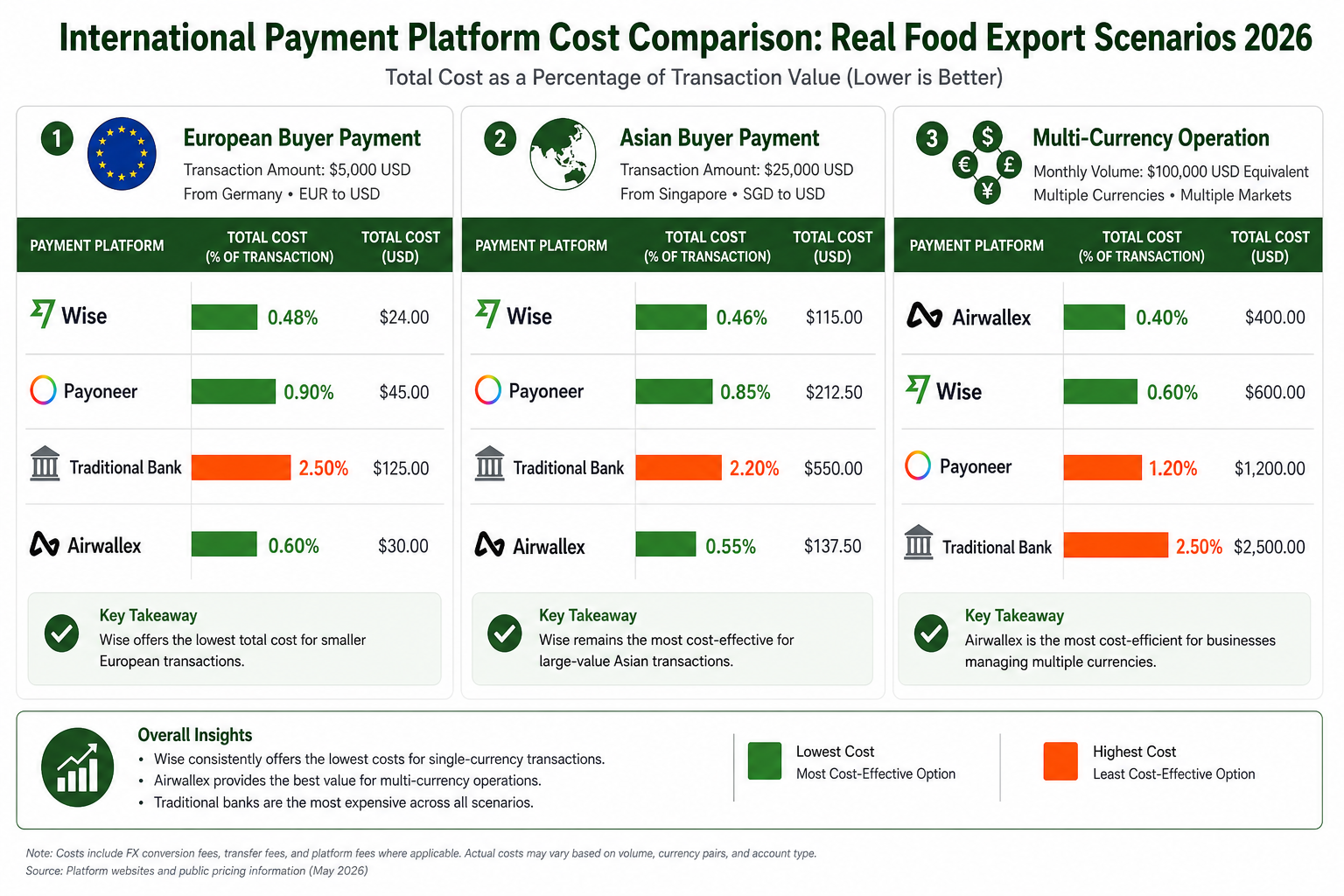

Scenario 1: European Buyer Pays €5,000

You're a Moroccan olive oil exporter. A French buyer pays your €5,000 invoice.

| Platform | Exchange Rate | Fee | Total Cost | You Receive |

|---|---|---|---|---|

| Wise | Mid-market (1.08) | 0.47% (€23.50) | €23.50 | $5,373 |

| Payoneer | 2% below mid-market (1.06) | 1% receiving fee (€50) | €50 + €100 conversion | $5,151 |

| Traditional Bank | 3% below mid-market (1.05) | $25 SWIFT + $15 intermediary | €40 + €150 conversion | $5,105 |

| Airwallex | Mid-market (1.08) | 0.3% (€15) | €15 | $5,382 |

Winner: Airwallex or Wise. Payoneer's combined receiving + conversion fees hurt on smaller transactions. Traditional banks cost nearly 6x more than Wise.

Scenario 2: Asian Buyer Pays $25,000

You're a Vietnamese coffee exporter. A Korean buyer pays your $25,000 invoice in USD.

| Platform | Exchange Rate | Fee | Total Cost | You Receive |

|---|---|---|---|---|

| Wise | N/A (USD to USD) | 0.39% ($97.50) | $97.50 | $24,902 |

| Payoneer | N/A (USD to USD) | 1% receiving ($250) | $250 | $24,750 |

| Traditional Bank | N/A (USD to USD) | $25 SWIFT + $15 intermediary | $40 | $24,960 |

| Airwallex | N/A (USD to USD) | 0.2% ($50) | $50 | $24,950 |

Winner: Traditional bank (surprisingly). On same-currency transactions, bank wire fees can be lower than percentage-based platforms. But this only works when your buyer pays in your currency — in practice, most buyers pay in their currency, triggering the exchange rate markup.

Scenario 3: Multi-Currency Operation

You export to 5 countries, receiving EUR, GBP, USD, AED, and JPY. You need to hold, convert, and spend in multiple currencies.

Winner: Wise Multi-Currency Account. You get local account details in 10+ currencies, letting buyers pay you as if you were a local business in their country. → Open Wise Business Account

For marketplace sellers (Alibaba, Amazon) who need to receive from platforms, Payoneer is the stronger choice — its marketplace integrations are deeper. → Sign up for Payoneer

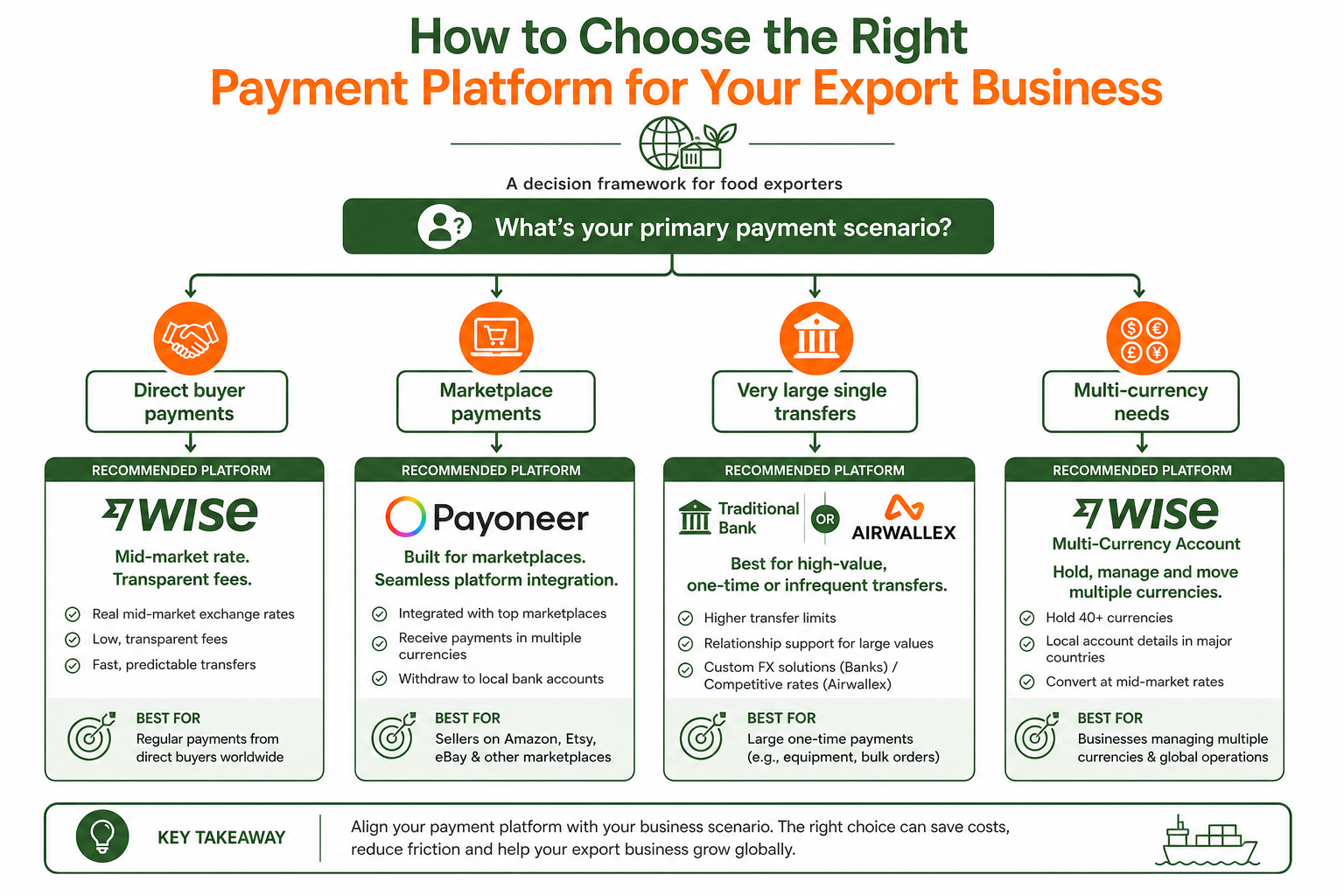

The Right Platform for Your Export Pattern

Use Wise if:

- You invoice buyers directly and receive payments in their local currency

- You want transparent pricing (see the fee before you accept)

- You operate in 5+ currencies and want local account details in each

- You're cost-sensitive and every percentage point matters

Cost: Free to open, no monthly fees. Pay per transaction (~0.4-0.6%). Business accounts have no minimum balance.

→ Open Wise Business Account (affiliate link — FoodExpoConnect earns a referral bonus)

Use Payoneer if:

- You sell through B2B marketplaces (Alibaba, TradeKey, Global Sources)

- You need a physical Mastercard for business expenses in multiple currencies

- You have a high volume of smaller transactions where the flat receiving fee is amortized

- You work with freelance suppliers or contractors internationally

Cost: Free to open. 1% receiving fee on most payments (marketplace payments may differ). Up to 2% currency conversion. $29.95 annual fee if you receive less than $2,000 in 12 months.

→ Sign up for Payoneer (affiliate link)

Use Airwallex if:

- You process $100,000+ annually in cross-border payments

- You want forward contracts to lock in exchange rates for 3-12 months

- You need corporate cards for team travel and trade show expenses

- You want the lowest percentage fees on high-volume transactions

Use a Traditional Bank if:

- Your buyer pays in your home currency (rare in food export)

- You're doing a single, very large transaction ($100,000+) where a flat wire fee beats percentage fees

- Your buyer requires a letter of credit (banks still dominate LCs)

Use a Combination (the Smart Strategy):

Most successful food exporters I work with use two platforms:

- Wise for buyer-direct payments (80% of transactions)

- Payoneer for marketplace payouts (15% of transactions)

- Bank for letters of credit and compliance documentation (5% of transactions)

This hybrid approach minimizes fees while covering all payment scenarios.

What About the Compliance Side?

International payments trigger compliance requirements. Here's what you need:

KYC (Know Your Customer): All platforms require business verification (incorporation documents, director ID, proof of address). This takes 2-5 business days. Do it before you need to receive a payment.

Transaction documentation: For payments over $10,000, most platforms will ask for the commercial invoice and sometimes the bill of lading. Keep these ready.

Tax reporting: If you receive more than $20,000 across 200+ transactions in a calendar year through a US payment processor, you'll receive a 1099-K. Non-US platforms (Wise is UK-based, Airwallex is Australia/Hong Kong) have different reporting thresholds. Consult your accountant.

Buyer verification: If a buyer sends you money from a sanctioned country or entity, the payment will be frozen. Screen your buyers before invoicing. A quick check against your government's sanctions list takes 5 minutes and saves weeks of frozen-funds headaches.

Beyond Payments: The Full Financial Stack

While you're optimizing payments, consider the other tools that make export finance manageable:

CRM for tracking buyer payments: If you're tracking payments in a spreadsheet, you're losing track of follow-ups. Pipedrive gives you a visual pipeline for each buyer relationship — and integrates with your email to auto-log communications. 20-30% commission for FoodExpoConnect referrals. → Start Pipedrive free trial

B2B contact data for buyer prospecting: Before you worry about getting paid, you need to find the buyers. Apollo.io has 275M+ verified B2B contacts with email finder — ideal for building targeted buyer lists. → Try Apollo.io free (60 credits/month)

Food safety compliance: Buyers increasingly require HACCP and FSSC 22000 documentation before they'll even discuss payment terms. FoodDocs digitizes your entire food safety system. → Start FoodDocs free trial

📊 Download the Payment Platform Fee Comparison →

Side-by-side fee comparison of Wise, Payoneer, and traditional banks across real food export payment scenarios. Know exactly which platform saves you the most on every transaction.

Free download — no email required.

The Bottom Line

If you do one thing after reading this: check your last three international payment receipts against the mid-market exchange rate. Calculate how much your bank actually charged you versus what Wise would have charged for the same transaction.

I've done this exercise with over 50 food exporters. The average savings from switching to Wise or Airwallex: $2,800 per year. For a small exporter operating on 15-20% margins, that's the equivalent of landing an extra $14,000-18,000 in sales.

And if you found this useful, the lead magnet below — our International Buyer Outreach Bundle — includes payment term templates in 6 languages, a buyer verification checklist, and our currency risk calculator. Free. Just drop your email.

Affiliate disclosure: FoodExpoConnect earns a commission when you sign up for Wise, Payoneer, Pipedrive, Apollo.io, or FoodDocs through the links in this article. This does not affect the price you pay. We only recommend products we've tested and that genuinely benefit food exporters.

Frequently asked questions

What's the cheapest way for food exporters to receive international payments?

Wise vs Payoneer: which is better for food exporters?

How much do traditional banks charge for international food export payments?

What payment methods do international food buyers prefer?

How do I handle currency exchange risk as a food exporter?

Quick facts

Published: 5/17/2026

Reading time: 14 min

Pillars: Payments, Cost Management

Written by

Jean Marc Koffi

Co-authorJournalist & Export SpecialistLondon

Jean Marc Koffi is an MBA-trained trade specialist who connects African exporters to global buyers, with over $20M in contracts facilitated and expertise recognized by major trade organizations. Noted for rapid buyer network building, he is an experienced speaker and certified in trade facilitation, origin rules, and food safety.

Alocha Massamba

Co-authorFounder, Epifresh & FoodExpoConnectLondon

Alocha Massamba is the founder of Epifresh and FoodExpoConnect. He builds the technology, data and partnerships that connect African food producers and exporters to international buyers — with a focus on fresh-produce supply chains, cold-chain logistics, and the buyer-discovery platforms small and mid-size exporters need to compete with global incumbents.

Series

More in Payments & FX for Exporters

International Payment Solutions for Food Exporters: Complete 2026 Comparison Guide

Compare the best international payment methods for food exporters. Learn about costs, speed, and features of traditional banks, Wise, PayPal, and specialized platforms to choose the right solution for your export business.

Explore more export intelligence

Coffee Export • Market Access • EU Regulations

Coffee Export 2026: African Origins, Fair Trade Pricing & EU Market Access

Complete guide to coffee export from Ethiopia, Kenya and Rwanda — EUDR compliance, fair trade pricing, certification requirements, and how to access €12-18/kg EU buyer contracts in 2026.

Market Access • Africa Trade • Export Strategy

China Zero-Tariff Policy for African Food Exporters: Coffee Imports Surge 145.7% — How to Enter the World's Largest Market Duty-Free

China's zero-tariff policy covering 53 African countries is already producing dramatic results — coffee imports surged 145.7% in the first five months. How food exporters can access this duty-free window and bypass traditional tariff barriers.

Export Operations • Finance • Middle East Trade

Payment Terms in the Middle East: LC, Cash Against Documents, Open Account (2026 Guide for Food Exporters)

Letters of credit, cash against documents, and open account each carry different risk profiles in Middle Eastern food trade. How to match payment terms to buyer relationships and country risk in Saudi Arabia, UAE, Qatar, and beyond.