FoodExpoConnect Blog

SeriesPayments & FX for ExportersInternational Payment Solutions for Food Exporters: Complete 2026 Comparison Guide

Compare the best international payment methods for food exporters. Learn about costs, speed, and features of traditional banks, Wise, PayPal, and specialized platforms to choose the right solution for your export business.

Introduction

Managing international payments is one of the biggest challenges food exporters face. Hidden bank fees, unfavorable exchange rates, and slow transfers can significantly impact your profit margins and cash flow. For small and mid-sized food export businesses, choosing the right payment solution can mean the difference between sustainable growth and struggling to stay profitable.

What you'll learn:

- How different international payment methods compare in cost, speed, and reliability

- The true cost of traditional bank transfers vs modern alternatives

- Which payment solution best fits your export business size and volume

- How to reduce payment fees by up to 85% on international transactions

- Key features to look for when evaluating payment providers

The Hidden Cost of Traditional Bank Transfers

Click to reveal the hidden costs

Most food exporters start by using their traditional bank for international payments. While familiar and seemingly straightforward, this approach often comes with significant hidden costs.

Understanding Bank Transfer Fees

Traditional banks typically charge fees in three ways:

- Transfer Fees: Flat fees ranging from $25-$50 per transaction

- Exchange Rate Markup: Banks add 3-6% above the mid-market exchange rate

- Intermediary Bank Fees: Additional $10-$30 charged by correspondent banks

Real-world example

Let's say you're a Nigerian cocoa exporter receiving €50,000 from a German buyer:

- Mid-market rate: €1 = ₦1,850

- Bank's rate: €1 = ₦1,740 (6% markup)

- Exchange rate loss: €50,000 × (₦1,850 - ₦1,740) = ₦5,500,000 ($3,500)

- Transfer fees: $45

- Total cost: ~$3,545 (7.1% of transaction)

Processing Times

Traditional bank transfers (SWIFT payments) typically take:

- 3-5 business days for major currency corridors (USD, EUR, GBP)

- 7-10 business days for less common routes

- Up to 15 days during holiday periods or for compliance reviews

For food exporters dealing with perishable goods, these delays can create cash flow challenges and complicate inventory management.

Modern Payment Solutions: A Comprehensive Comparison

The fintech revolution has brought numerous alternatives to traditional banking. Here's how the major players compare for food export businesses.

1. Wise (formerly TransferWise)

Click to view Wise details (Cost, Speed, Features)

Overview

Best for: Regular international payments, multi-currency needs

How it works

Wise uses a peer-to-peer model that matches transfers going in opposite directions, avoiding traditional SWIFT networks. This allows them to offer the real mid-market exchange rate with transparent fees.

Cost Structure

- Exchange rate: Mid-market rate (0% markup)

- Transfer fee: 0.41% - 2.0% depending on currency pair and payment method

- No hidden fees: What you see is what you pay

Example cost

(Based on €50,000 transfer from Germany to Nigeria)

- Mid-market rate applied: €50,000 × ₦1,850 = ₦92,500,000

- Transfer fee (0.75%): €375 ($400)

- Total cost: ~$400 (0.8% of transaction)

- Savings vs bank: $3,145 (88% cheaper)

Processing time

- Major currencies: 1-2 business days

- Emerging markets: 2-4 business days

Key features

- Multi-currency account: Hold and manage 50+ currencies

- Local bank details: Get local account numbers in USD, EUR, GBP, AUD, etc.

- Batch payments: Send multiple payments at once

- API integration: Automate payments via API

- Business debit card: Spend in multiple currencies

- Accounting software integration: Connects with QuickBooks, Xero

Limitations

- Not available in all countries

- Some currency routes have higher fees

- Cash deposit/pickup not available

- May require business verification documents

Best suited for

- Exporters with monthly volume of $10,000+

- Businesses dealing with multiple currencies

- Companies seeking transparency and low fees

2. PayPal Business

Click to view PayPal details (Cost, Speed, Features)

Overview

Best for: Small transactions, buyers who prefer PayPal checkout

Cost Structure

- International sales: 4.4% + fixed fee (varies by currency)

- Currency conversion: 3-4% above mid-market rate

- Withdrawal fees: Free for bank transfers in most countries

Example cost

(Based on €50,000 transfer)

- Currency conversion markup: ~€1,500 ($1,600)

- Transaction fee (4.4%): €2,200 ($2,350)

- Total cost: ~$3,950 (7.9% of transaction)

Processing time

Instant for PayPal-to-PayPal, 3-5 days for bank withdrawal

Key features

- Buyer/seller protection: Dispute resolution system

- Invoicing: Send professional invoices

- Global reach: Accepted in 200+ countries

- Easy integration: Simple payment buttons for websites

Limitations

- High fees for large transactions

- Account holds/freezes can occur

- Limited currency support for holds (25 currencies)

- Dispute process can favor buyers

Best suited for

- Small exporters (<$5,000/month volume)

- Businesses selling to consumers (B2C)

- One-time or occasional international sales

3. Western Union Business Solutions

Click to view Western Union details (Cost, Speed, Features)

Overview

Best for: Cash-based markets, urgent transfers

Cost Structure

- Fees: Negotiated based on volume, typically 1-3%

- Exchange rate markup: 2-4% above mid-market

Example cost

(Based on €50,000 transfer)

- Exchange rate markup: ~€1,500 ($1,600)

- Transfer fee (2%): €1,000 ($1,070)

- Total cost: ~$2,670 (5.3% of transaction)

Processing time

Same-day to 1 business day

Key features

- Cash pickup: Receiver can collect cash at 500,000+ locations

- Dedicated account manager: For business accounts

- Hedging tools: Lock in exchange rates for future payments

- Risk management: Compliance and fraud protection

Limitations

- Higher fees than Wise for standard transfers

- Requires business account setup

- May have minimum volume requirements

Best suited for

- Exporters working with buyers in cash-based economies

- Time-sensitive payments (same-day delivery needed)

- Businesses with high monthly volume ($100,000+)

4. Revolut Business

Click to view Revolut details (Cost, Speed, Features)

Overview

Best for: European and UK exporters, expense management

Cost Structure

- Exchange rate: Inter-bank rate for major currencies

- Transfer fees: Vary by plan (€0-€30 per transfer)

- Monthly subscription: €25-€100 depending on plan

Key features

- Multi-currency accounts: 30+ currencies

- Corporate cards: With spending controls

- Expense management: Built-in tools

- Integrations: Connects with accounting software

Limitations

- Limited coverage in Africa and Latin America

- Some features require higher-tier plans

- Customer support varies by plan level

Best suited for

- EU/UK-based food exporters

- Teams needing expense management tools

- Businesses wanting all-in-one financial platform

5. Payoneer

Click to view Payoneer details (Cost, Speed, Features)

Overview

Best for: Receiving payments from marketplaces and platforms

Cost Structure

- Receiving payments: 0-3% depending on source

- Currency conversion: Up to 2% markup

- Bank withdrawal: $1.50 flat fee

Key features

- Marketplace integration: Easy setup for Amazon, Alibaba, etc.

- Multi-currency receiving accounts: USD, EUR, GBP, JPY, CNY

- Mass payout services: Pay multiple suppliers/partners

- Prepaid Mastercard: Access funds anywhere

Limitations

- Higher fees for card payments

- Limited business tools compared to Wise

- Customer service response times vary

Best suited for

- Exporters selling on B2B marketplaces

- Receiving payments from multiple sources

- China trade corridor

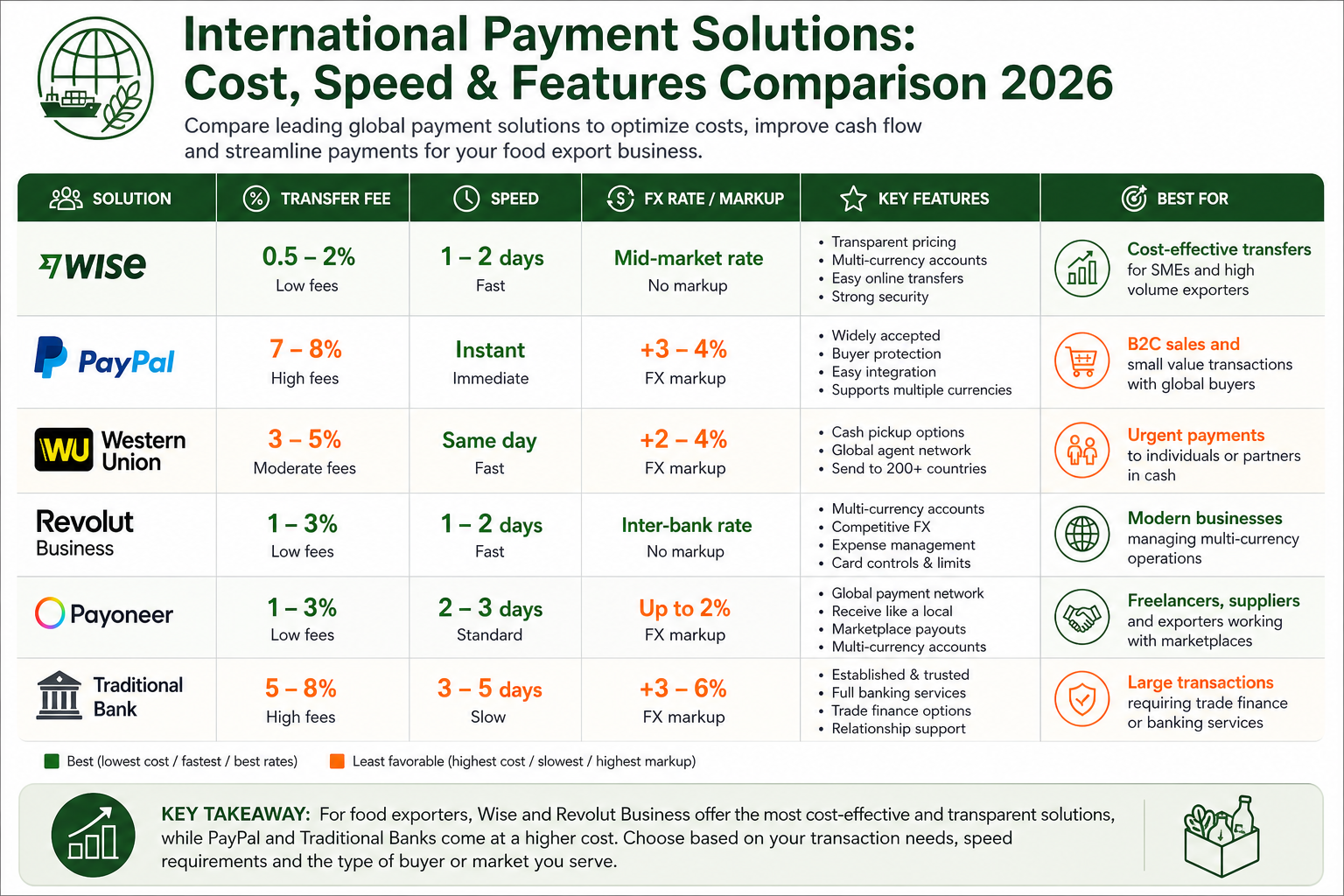

Comparison Table: Quick Reference

Click to view comparison table

| Provider | Best For | Avg. Cost | Speed | Multi-Currency Account | API Available |

|---|---|---|---|---|---|

| Traditional Bank | Large transfers (>$500k) | 5-8% | 3-5 days | No | Limited |

| Wise | Regular transfers, transparency | 0.5-2% | 1-2 days | Yes (50+ currencies) | Yes |

| PayPal | Small amounts, buyer protection | 7-8% | Instant | Limited (25 currencies) | Yes |

| Western Union | Cash markets, urgent | 3-5% | Same day | No | Yes |

| Revolut Business | EU/UK businesses | 1-3% | 1-2 days | Yes (30+ currencies) | Yes |

| Payoneer | Marketplace payments | 1-3% | 2-3 days | Yes (5 currencies) | Yes |

Choosing the Right Solution for Your Export Business

The best payment solution depends on your specific needs. Here's a decision framework:

By Business Size

Click to view recommendations by business size

Small exporters (<$50,000/year)

- Primary: Wise for transparency and low fees

- Backup: PayPal for buyers who insist on it

Medium exporters ($50,000-$500,000/year)

- Primary: Wise for most transactions

- Specialized: Western Union for cash markets

- Consider: Revolut Business if EU-based

Large exporters (>$500,000/year)

- Primary: Wise or negotiate rates with traditional bank

- Hedging: Western Union Business Solutions for FX risk management

- Multi-tool: Use different providers for different routes

By Geographic Focus

Click to view recommendations by region

Exporting to EU/UK

- Wise (excellent coverage, local IBANs)

- Revolut Business (if based in EU)

Exporting to USA

- Wise (US ACH routing numbers available)

- Payoneer (if selling on US marketplaces)

Exporting to Middle East/North Africa

- Western Union (strong cash network)

- Wise (growing coverage in UAE, Egypt)

Exporting to Asia

- Payoneer (strong China corridor)

- Wise (good coverage for Singapore, Hong Kong, Japan)

By Payment Frequency

Click to view recommendations by frequency

Regular monthly payments

- Wise (best for predictable, recurring transfers)

- Set up automated payments via API

Occasional/seasonal

- PayPal (pay-as-you-go, no monthly fees)

- Traditional bank (if already established relationship)

High-frequency daily

- Wise API with automation

- Consider dedicated account manager at Western Union

How to Set Up Wise for Your Food Export Business

Click to view setup guide

Since Wise offers the best combination of low fees, transparency, and features for most food exporters, here's a step-by-step setup guide:

Step 1: Create Your Wise Business Account

1. Visit wise.com/business and click "Get Started"

2. Provide your business details:

- Business legal name and registration number

- Business address and tax ID

- Industry (select "Food & Beverage" or "Agriculture")

- Estimated monthly volume

3. Verify your identity:

- Government-issued ID (passport or driver's license)

- Proof of address (utility bill or bank statement)

4. Verify your business:

- Certificate of incorporation

- Proof of business address

- Shareholder information (if applicable)

Verification time: 1-3 business days

Step 2: Activate Currency Accounts

1. Navigate to "Balances" in your Wise dashboard

2. Click "Open a balance" for each currency you need

3. Get local bank details instantly for:

- USD (ACH routing number)

- EUR (IBAN)

- GBP (Sort code + account number)

- AUD, NZD, CAD, and 40+ more

Use case: Share these local account numbers with your international buyers so they can pay you as if you're a local business, avoiding their international transfer fees.

Step 3: Make Your First Transfer

1. Click "Send" in your Wise dashboard

2. Enter:

- Amount and currency

- Recipient details (bank account or Wise account)

- Purpose of payment (for compliance)

3. Review the breakdown:

- Exact exchange rate (always mid-market)

- Transfer fee (fixed percentage)

- Expected delivery time

4. Fund the transfer via:

- Bank transfer (cheapest)

- Debit card (instant, small fee)

- Existing Wise balance

Pro tip: Fund transfers via bank transfer to avoid debit card fees. For urgent payments, card funding is worth the small extra cost for instant processing.

Step 4: Integrate with Your Accounting Software

1. Go to "Settings" → "Integrations"

2. Connect your accounting software:

- Xero

- QuickBooks

- FreeAgent

- Or use CSV export for other systems

3. Enable automatic transaction sync

Benefit: Eliminate manual reconciliation and reduce accounting time by 70%.

Step 5: Set Up the Wise Business Debit Card

1. Order your Wise Business debit card (free)

2. Receive it within 7-10 business days

3. Use it to:

- Pay for trade show expenses in local currency

- Make supplier payments abroad

- Withdraw cash at ATMs worldwide (up to $200/month free)

Advantage: Card automatically converts at mid-market rate when you spend in foreign currency—no 3% credit card foreign transaction fees.

Step 6: Enable API Access (Optional, for High-Volume Exporters)

1. Contact Wise to request API access

2. Integrate with your ERP/accounting system

3. Automate:

- Batch payments to multiple suppliers

- Regular payment schedules

- Currency conversions based on triggers

Reducing Payment Costs: Advanced Strategies

1. Timing Your Transfers

Learn about timing strategies

Exchange rates fluctuate constantly. For large transfers:

- Use rate alerts: Set up notifications when your target rate is reached (available in Wise)

- Consider forward contracts: Lock in a rate for future payments (available through Western Union Business Solutions or specialized FX brokers)

- Avoid weekends: Exchange rate spreads are wider when markets are closed

2. Optimize Payment Terms

Learn about payment terms optimization

Negotiate with buyers to:

- Accept local currency payments: Use your Wise local bank details to receive payments in your buyers' currencies, then convert on your schedule

- Net payment terms: Batch multiple smaller invoices into one larger monthly payment to reduce per-transaction costs

- Prepayment discounts: Offer 2-3% discount for advance payment to improve cash flow and reduce currency risk

3. Multi-Currency Strategy

Learn about multi-currency strategies

Hold balances in your major trading currencies:

1. Identify your top 3 currencies by volume (e.g., EUR, USD, GBP)

2. Keep working capital in these currencies (~1-2 months of expenses)

3. Convert strategically when rates are favorable, not when you need the money urgently

4. Pay suppliers directly in their currency without double conversion

Example

If you're a Ghanaian cashew exporter selling to EU buyers and buying raw nuts from Ivory Coast:

- Receive EUR payments → Hold in EUR balance

- Pay Ivorian suppliers in XOF (West African CFA franc)

- Convert EUR → XOF only when needed at favorable rates

- Avoid unnecessary GHS (Ghana Cedi) conversions

4. Leverage Volume Discounts

Learn about volume discounts

For exporters with monthly volumes exceeding $100,000:

- Negotiate with Wise: Contact their team for reduced fees on high volumes

- Western Union Business Solutions: Dedicated rates for regular clients

- Traditional banks: Use your volume as leverage to negotiate better rates

- Specialized FX brokers: Consider OFX, TorFX, or Currencies Direct for very large transfers

Common Mistakes to Avoid

1. Not Calculating Total Cost

View mistake details

Mistake

Comparing only transfer fees without considering exchange rate markups.

Solution

Always calculate the total cost as a percentage of the transfer amount. Use comparison tools like Wise's calculator to see the full picture.

2. Using Credit Cards for International Payments

View mistake details

Mistake

Paying foreign suppliers with credit cards due to convenience.

Problem

Credit card foreign transaction fees (3%) + cash advance fees (5%) + interest can exceed 10% total cost.

Solution

Use Wise or bank transfer for B2B payments. Reserve credit cards only for small, urgent purchases where the reward points offset the fees.

3. Not Diversifying Payment Providers

View mistake details

Mistake

Relying on a single payment method.

Risk

If your primary provider has downtime, compliance holds, or doesn't support a specific route, your business operations stop.

Solution

Have at least two payment providers set up and tested. For example:

- Primary: Wise (for 90% of transactions)

- Backup: PayPal or traditional bank (for when Wise doesn't support a route)

4. Ignoring Compliance Requirements

View mistake details

Mistake

Providing incomplete or inconsistent documentation.

Consequence

Payment delays, account holds, or rejected transfers.

Solution

- Keep digital copies of all invoices and contracts

- Provide clear purpose of payment descriptions

- Maintain consistent business information across all platforms

- Respond promptly to verification requests

5. Converting Currency Too Many Times

View mistake details

Mistake

USD → EUR → GBP → USD conversions lose money at each step.

Solution

- Hold balances in your actual trading currencies

- Pay directly in recipient's currency when possible

- Use multi-currency accounts to avoid round-tripping

Tax and Compliance Considerations

Record Keeping

What records do you need to keep?

For tax purposes, maintain records of:

- All international transfers: Amount, date, exchange rate used, fees paid

- Invoices and contracts: Proving the commercial purpose of each payment

- Exchange rate documentation: For calculating tax liability in your local currency

Pro tip: Wise automatically provides detailed statements with all this information, making year-end tax filing much easier.

Reporting Requirements

What are the reporting requirements?

Depending on your country, you may need to report:

- Foreign exchange transactions above certain thresholds to central banks

- Foreign currency holdings in annual tax returns

- International payments to trade/customs authorities

Example

In Nigeria, the CBN requires exporters to repatriate export proceeds within 90 days. Wise transfers provide audit trails proving compliance.

Anti-Money Laundering (AML) Compliance

Understanding AML compliance

All reputable payment providers will:

- Verify your business identity and beneficial owners

- Ask for source of funds documentation

- Monitor transactions for suspicious activity

- Report large or unusual transactions to authorities

What you need

- Clear documentation of your export business (contracts, invoices, shipping documents)

- Transparent ownership structure

- Consistent transaction patterns matching your business model

Frequently Asked Questions (FAQ)

Can I use my personal bank account for export business?

While possible for very small starts, it's not recommended. Personal accounts often have lower transaction limits, higher fees for international transfers, and lack essential business features like multi-currency holding. Plus, it looks unprofessional to international buyers.Which currency should I invoice in?

Ideally, invoice in a major currency (USD, EUR, GBP) that your buyer is comfortable with. If you use a multi-currency account like Wise, you can provide local bank details for these currencies, making it easier for buyers to pay you without them incurring international wire fees.How do I protect myself from exchange rate fluctuations?

For short-term protection, use limit orders (auto-convert when rate hits a target). For long-term contracts, consider "forward contracts" offered by providers like Western Union Business Solutions, which allow you to lock in an exchange rate for a future date.Are fintech banks like Wise safe?

Yes. Reputable fintechs are regulated by the same financial authorities as traditional banks (e.g., FCA in the UK, FinCEN in the US). They are required to safeguard customer funds in separate accounts from their own operating capital.📥 Export Payment Checklist

Don't lose money on your next shipment. Download our free 10-point checklist to ensure you're using the most cost-effective payment method.

- Compare mid-market vs. bank rates

- Verify hidden intermediary fees

- Check compliance document requirements

🌍 Find Verified International Buyers

Ready to export but need reliable partners? Access our directory of 500+ verified food importers across Europe, Asia, and North America.

Access Buyer Directory💳 Get the Payment Implementation Planner →

Step-by-step implementation guide for integrating Wise, Payoneer, or traditional bank solutions into your export payment workflow. Fee comparison tables, settlement time analysis, and multi-currency account setup checklist.

Free download — no email required.

Conclusion: Making the Switch

For most small and mid-sized food exporters, switching from traditional banks to modern payment platforms like Wise can result in:

- Cost savings of 70-90% on international transfer fees

- Faster payment processing (1-2 days vs 5-7 days)

- Better cash flow management with multi-currency accounts

- Simplified accounting through software integrations

- Greater transparency with real-time tracking and no hidden fees

Your Action Plan

This week

- Calculate your current annual cost of international payments (fees + exchange rate markups)

- Sign up for a Wise business account (or your chosen alternative)

- Make one test transfer to verify the process and timing

This month

- Migrate 50% of your international payments to your new provider

- Set up local currency accounts for your top 3 trading partners

- Integrate with your accounting software

This quarter

- Analyze cost savings achieved vs traditional banking

- Optimize your currency holding strategy based on actual payment patterns

- Train your finance team on the new platform

Long-term

- Negotiate better rates based on proven volume

- Explore API integration for automation

- Consider forward contracts for large, planned future payments

Need More Help?

International payments are just one piece of successfully scaling your food export business. At FoodExpoConnect, we help African and emerging market food exporters connect with verified international buyers, navigate export regulations, and build sustainable global trade relationships.

Explore our resources

- How to Find International Food Buyers: 7 Proven Strategies

- Complete Guide to Food Export for African Businesses 2025

- Food Safety Certifications for Export: HACCP, ISO 22000, FSSC 22000 Explained

Disclaimer: This article is for educational purposes and does not constitute financial advice. Exchange rates, fees, and features of payment providers are subject to change. Always verify current rates and terms with providers before making decisions. FoodExpoConnect may earn affiliate commissions from some of the providers mentioned when you sign up through our referral links, at no extra cost to you.

Quick facts

Published: 12/16/2025

Reading time: 12 min

Pillars: export-success

Written by

Jean Marc Koffi

Co-authorJournalist & Export SpecialistLondon

Jean Marc Koffi is an MBA-trained trade specialist who connects African exporters to global buyers, with over $20M in contracts facilitated and expertise recognized by major trade organizations. Noted for rapid buyer network building, he is an experienced speaker and certified in trade facilitation, origin rules, and food safety.

Alocha Massamba

Co-authorFounder, Epifresh & FoodExpoConnectLondon

Alocha Massamba is the founder of Epifresh and FoodExpoConnect. He builds the technology, data and partnerships that connect African food producers and exporters to international buyers — with a focus on fresh-produce supply chains, cold-chain logistics, and the buyer-discovery platforms small and mid-size exporters need to compete with global incumbents.

Series

More in Payments & FX for Exporters

Best Payment Platforms for Food Exporters in 2026: Wise vs Payoneer vs Banks (Real Fee Comparison)

International payment fees quietly eat 3-7% of your export revenue. We tested Wise, Payoneer, and traditional banks with real transaction scenarios. Here's which platform saves you the most money — and when to use each one.

Explore more export intelligence

Certification • Pricing Strategy • Market Access

5 Certifications Worth More Than a Price Cut in 2026

Stop competing on price. Organic, Fair Trade, Rainforest Alliance, B Corp, and SQF certifications can command 20-300% price premiums for African food exporters in 2026. Here is the ROI data for each.

Coffee Export • Market Access • EU Regulations

Coffee Export 2026: African Origins, Fair Trade Pricing & EU Market Access

Complete guide to coffee export from Ethiopia, Kenya and Rwanda — EUDR compliance, fair trade pricing, certification requirements, and how to access €12-18/kg EU buyer contracts in 2026.

Market Access • Africa Trade • Export Strategy

China Zero-Tariff Policy for African Food Exporters: Coffee Imports Surge 145.7% — How to Enter the World's Largest Market Duty-Free

China's zero-tariff policy covering 53 African countries is already producing dramatic results — coffee imports surged 145.7% in the first five months. How food exporters can access this duty-free window and bypass traditional tariff barriers.